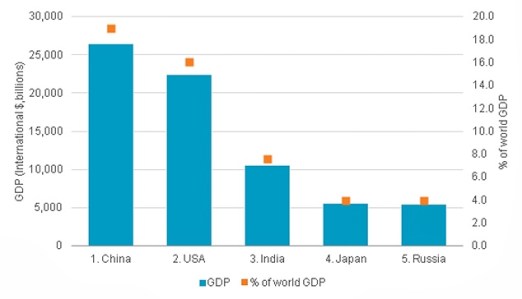

Source: Euromonitor International from national statistics/Eurostat/OECD/UN/International Monetary Fund (IMF), International Financial Statistics (IFS)Note: Purchasing Power Parity has been used as this is a method of measuring the relative purchasing power of different countries’ currencies over the same types of goods and services, thus allowing a more accurate comparison of living standards.

By 2020, three of the world’s five largest economies will be emerging countries, accounting for 30.4% of global GDP in PPP terms. Advanced economies are being displaced by emerging market superpowers, notably the BRIC countries, which has been accelerated by the seismic effects of the global economic downturn of 2008-2009. Euromonitor International predicts that China will become the world’s largest economy in PPP terms in 2017.

Additionally, Russia will overtake Germany as the fifth largest economy in 2016. These shifts will influence global politics, business environments and investment flows while consumer markets in developing countries will rise in importance as the middle class expands.

1. China: Set to become world’s largest economy in 2017

A large manufacturing base, cheap labour costs, the world’s largest population and economies of scale have resulted in unprecedented economic growth in China. Although growth is slowing, the delayed recovery in advanced economies from the global economic downturn means China will overtake the USA as the world’s biggest economy in 2017, and account for 19.0% of global GDP in PPP terms by 2020. Challenges loom large, however, including rising labour costs, pollution, a potential real estate bubble and rapid ageing arising from the government’s one child policy. Euromonitor predicts that China’s working age population (aged 15-64) will decline from 2014.

2. USA: End of the American dream?

The USA will lose its position as the world’s number one economy in 2017. In 1990, the USA accounted for a quarter of global GDP in PPP terms but we forecast this to plummet to 16.0% by 2020. The country was where the global financial crisis began in 2008 and it has failed to recover to its potential while also slipping in global competitiveness rankings. Although the government avoided the “fiscal cliff” in 2012, one of the biggest challenges remains a budget deficit reduction strategy, without the ensuing political gridlock. Nevertheless, the USA retains advantages, namely as the world’s largest consumer market and a leader of technological innovation.

3. India: Demographic dividend to benefit country beyond 2020

India overtook Japan as the world’s third largest economy in PPP terms in 2011 and its demographic advantage means the country could become the world’s biggest economy in the coming decades. India has a young population where it is benefitting from its demographic dividend (when there are more people of working age and the proportion of the child population declines). Euromonitor forecasts that India will become the world’s largest population by 2025 and that its working-age population will increase by 11.6% in 2013-2020 compared to -3.1% in China. However, India lags in major indicators including educational attainment and infrastructure development.

4. Japan: Paying the price for decades of economic stagnation

Structural problems beset Japan, with decades of weak economic growth and deflation while it has totalled the highest proportion of public debt in the world at 235% of GDP in 2012. Although the country has not yet suffered a eurozone-style sovereign debt crisis, as the majority of its debt is domestically-owned, an increase of foreign debt could trigger a Japanese debt crisis. It has the oldest population globally (mean age of 44.7 in 2012) and a shrinking labour force which will add considerable strain on government finances, while a strong currency makes its exports uncompetitive. Yet Japan’s location within Asia means it can take advantage of cheaper production costs in the region and growing demand for its high-tech products from a burgeoning Asian middle class. Like the USA, it is a global technological leader, giving it a competitive edge over its emerging neighbours.

5. Russia: Overtakes Germany as fifth largest economy in 2016

Russia will become the world’s fifth largest economy in 2016 in PPP terms, driven by its energy sector, as one of the top oil and natural gas producers worldwide. It also offers potential in its rapidly expanding consumer market, which Euromonitor forecasts will be the ninth largest globally in real terms in 2020. Its accession to the World Trade Organisation in August 2012 further cements its integration into the global economy. The lack of economic diversification and modernisation remain key long-term challenges with government policy aiming to tackle this, for example, by investing in the Skolkovo Innovation Centre Project, Russia’s equivalent to Silicon Valley. Corruption, state control and bureaucracy also hamper the business environment in Russia. Like elsewhere in Eastern Europe, the Russian working-age population is in decline (-4.5% in 2013-2020) despite a short-term baby boom, which will pose a demographic challenge to sustaining non-oil economic growth. Source: Euromonitor.com

You must be logged in to post a comment.