Madagascar’s customs authority is currently receiving technical support from the International Monetary Fund (IMF) to accelerate its digital transformation. Two specialists, Victor Budeau and François Chastel, began their mission in Antananarivo on Thursday, April 24th. Their assignment, scheduled to conclude on Wednesday, May 7th, includes intensive training focused on incorporating artificial intelligence (AI) into customs procedures.

The objective is to improve the efficiency, accuracy, and transparency of operations. During a working session, the Director General of Customs, Ernest Zafivanona Lainkana (pictured, center), underscored the significance of centralizing data within a unified database to fully harness the potential of AI. He also affirmed that this technology must now become a fundamental component of customs tools.

This initiative is not merely an experiment but rather part of an ongoing strategy. The customs administration is already using several AI-driven solutions: automatic image analysis (RESNET), Smart Scanning, and the Enhanced Risk Assessment (ERA) system. These tools have contributed to a 68% increase in customs revenues in January 2025 compared to January 2024.

Given these positive outcomes, the IMF has designated Madagascar as a pilot project in Africa for the integration of AI into customs services. This strategic recognition could lay the foundation for a continent-wide strategy. By 2029, Madagascar’s customs authority aims to extend these technologies to additional control sectors, strengthen its digital infrastructure, and share its expertise at the regional level.

The following article featured in the 1st Issue of the WCO Newsletter 2023. It is authored by Anthony Buckley, Chair of Customs Knowledge Institute. The article argues that a formal plan for building and managing Customs knowledge is necessary for a Customs brokerage to operate effectively. The components of such a plan are discussed, as well as the determinants that may affect the choices made. The discussion refers also to general issues of Customs knowledge acquisition, management and updating. The considerations apply to all Customs practitioners and trading businesses.

The number of possible games of chess is greater than the number of atoms in the observable universe according to Claude Shannon. In Customs, there are many more variables than the 32 pieces on a chessboard. In any transaction, we have the interested parties, the type of transaction, the goods involved, the route being followed, the intended procedure, the non-tariff controls, the rates of duty and the liability for payment, each of them with many possible variations, combinations, and types of supporting evidence. On that basis, it seems that every single movement of goods across a Customs border is unique, at least in some minor way. How does a Customs broker meet the expectation of a client, who expects the broker to be familiar with every possible variation?

As if the challenge of complexity is not enough, the broker is also expected to maintain records of all transactions and retrieve them in various formats as required by customers and Customs administrations.

In practice, of course, we find ways of doing things that are theoretically impossible. Most Customs movements fall into certain categories and are handled accordingly, by operators familiar with one or a few of the categories. High value complex transactions are handled by teams with a mix of expertise, at considerable expense. Low value consignments use simplified procedures and reduced checking. Significantly, evidence[1] suggests that many transactions proceed despite errors, sometimes of significant effect. Thus, when considering “Customs knowledge”, we must distinguish between what is necessary for all, and what is essential only for certain functions.

All economic operators must have a general understanding of what Customs is, how it controls trade, what its legal structure is, what rights, entitlements and obligations attach to the operator and to the Customs authorities, the importance of compliance with legal requirements, and the costs of non-compliance. For many who buy and sell internationally, their knowledge does not proceed far beyond this general understanding, except perhaps for some detail concerning the particular goods they trade.

For a Customs broker, this level of knowledge is only the beginning.

The 26th/27th Meetings of the SAFE Working Group (SWG) were held successfully from 11 to 14 April 2022. The virtual meetings brought together more than 260 delegates representing Customs administrations, the Private Sector Consultative Group (PSCG), other international organizations and academia.

In his opening remarks, Mr. Pranab Kumar Das, WCO Director of Compliance and Facilitation, highlighted that the SWG had reached an important juncture as the new three-year SAFE review cycle 2021-2024 was about to enter into discussions. It was pointed out that 17 years after it was first published, the SAFE Framework of Standards (FoS) had garnered substantial interest from WCO Members. During the meetings, Guyana became the 172nd WCO Member to express its interest in implementing the SAFE FoS.

With a view to continued enhancement of the AEO criteria and provisions to strengthen the SAFE FoS, WCO Members made several new proposals to revise the Framework. The SWG also received feedback from the private sector on the urgent need to enhance the harmonization of SAFE and AEO implementation. In this context, the SWG heard a presentation by the WCO Anti-Corruption and Integrity Promotion (A-CIP) Programme on maintaining the integrity and transparency of AEO implementation.

On this occasion, the SWG reviewed and adopted the new Work Plan for 2022-2024, which reflected the critical activities the SWG will carry out over the next two years until 2024, in parallel with the SAFE review cycle. The SWG also received an update on the development of new features for the Online AEO Compendium (OAC) and the other extensive work underway in collaboration with other international organizations in the areas of security and facilitation.

Against the backdrop of the WCO’s theme for 2022, the panel discussion on “Scaling up Customs Digital Transformation by Embracing a Data Culture and Building a Data Ecosystem” attracted significant interest from Members and the private sector. The experienced speakers from Member Customs administrations, the private sector and the Secretariat enriched the discussions by sharing their best practices on using data for enhancing risk management and monitoring AEO programmes.

As a way forward, the SWG agreed that efforts will be reserved for a comprehensive review to assess and monitor SAFE implementation for greater harmonization of AEO programmes globally.

The WCO and the World Trade Organization (WTO) held a webinar to launch their joint publication on Customs use of advance technologies. The event attracted more than 700 attendees and provided insights into how advanced technologies can help Customs administrations facilitate the flow of goods across borders. The publication titled, “The role of advanced technologies in cross-border trade: A customs perspective” provides the current state of play and sheds light on the opportunities and challenges Customs face when deploying these technologies.

The publication outlines the key findings of WCO’s 2021 Annual Consolidated Survey and its results on Customs’ use of advanced technologies such as blockchain, the internet of things, data analytics and artificial intelligence to facilitate trade and enhance safety, security and fair revenue collection.

The joint publication highlights the benefits that can result from the adoption of these advanced technologies, such as enhanced transparency of procedures, sharing of information amongst all relevant stakeholders in real time, better risk management, and improved data quality, leading to greater efficiency in Customs processes and procedures.

In his remarks, WCO Deputy Secretary General Ricardo Treviño Chapa said, “Technologies will assist implementation of international trade facilitation rules and standards, such as the WCO Revised Kyoto Convention and the WTO Trade Facilitation Agreement. We are therefore delighted to be partnering with the WTO, to ensure that our work in assisting our Members’ digital transformation journeys is complementary, that we bring all relevant partners to the same table, and that we avoid duplication.”

In her opening remarks, WTO Deputy Director-General Anabel González noted, “Advanced technologies offer customs an opportunity to take a big leap forward on trade facilitation. Take blockchain. Its widespread application could help us make trade both more transparent and less paper intensive. That would reduce trade costs, which is good news for everyone, especially small businesses, which are disproportionately affected by red tape at the border.”

The webinar presented the main findings from the WCO/WTO paper and featured presentations by Brazil, Nigeria, Singapore and the Inter-American Development Bank. For a greater uptake of these technologies, the speakers underlined the importance of continuous sensitization of Customs and other stakeholders, the need for interoperability and implementation of international standards, the relevance of engaging in dialogues at international level, as well as having a strategy and space for innovation and testing at national level.

Herewith a 2020 update of the ICC BASCAP report assessing the environment and highlighting trends in counterfeiting and other forms of illicit trade facilitated within free trade zones.

The Risks

Free Trade Zones (FTZs) provide significant opportunities for legitimate business and play a critical role in global trade as well as economic growth for the host nation. However, our updated research has continued to confirm that insufficient oversight remains a major enabler of illicit activities. Since the publication of our previous 2013 report, there have not been vast improvements in limiting criminal activities within FTZs. In fact, the Covid-19 pandemic has increased vulnerability for abuses by criminal actors who take advantage of supply chain shortages and increased demands as well as relaxed oversight often because of such things as quarantines that have softened Customs control.

Counterfeiters use transit or transhipment of goods, through multiple, geographically diverse FTZs for no other purpose than to disguise the illicit nature of the products. Once introduced into an FTZ, counterfeit goods may undergo a series of economic operations, including assembly, manufacturing, processing, warehousing, re-packaging, and re-labelling. Once completed, the goods can be imported directly to the national territory of the hosting state or re-exported to another country for distribution or to another FTZ, where the process is repeated.

Key recommendations:

Our 2020 report promotes a set of specific policy and legislative recommendations on how to preserve and expand the benefits of FTZs for legitimate traders and protect the public and honest businesses from predatory practices. These recommendations are based on a review of the international and national legal frameworks governing FTZs, including how they are implemented and enforced.

Suggested recommendations include:

empowering Customs with jurisdiction over day-to-day operations within FTZs

strengthening relationship between Customs and FTZs

clarifying and declaring that FTZs remain under the jurisdiction of the national Customs authority

enhancing data sharing between Customs and the private sector

strengthening national government adherence to international conventions and implementation of international standards

legislatively ensuring that strict penalties are in place, including criminal sanctions where appropriate, against perpetrators of illegal activities in FTZs

that manufacturers and shippers recognize and use the ICC World Chambers Foundation’s International Certificates of Origin (COs) Accreditation Chain which is a program that accredits chambers of commerce issuing COs wishing to guarantee their commitment to the highest level of quality, implementing transparent and accountable issuance and verification procedures. Accredited chambers will receive a distinctive internationally recognized quality classification, reinforcing their integrity and credibility as competent trusted third parties in the issuance of COs.

Additionally, the new document also provides specific recommendations such as drawing on international agreements, lessons learned from effective and ineffective national legislation, the experience of IP rights holders, and legislative and regulatory measures to enforce intellectual property right protection in FTZs. These specific recommendations are delineated in the report for action by the World Customs Organization, World Trade Organization, national governments, and FTZ operators. Effective implementation of the measures delineated for each of these bodies will go a long way in securing FTZs from illicit traders.

From 1 January 2021, the transition period with the European Union (EU) will end, and the United Kingdom (UK) will operate a full, external border as a sovereign nation. This means that controls will be placed on the movement of goods between Great Britain (GB) and the EU.

The UK Government will implement full border controls on imports coming into GB from the EU. Recognising the impact of coronavirus on businesses’ ability to prepare, the UK Government has taken the decision to introduce the new border controls in three stages up until 1 July 2021.

Her Majesty’s Revenue & Customs (HMRC) published the first iteration of the Border Operating Model in July 2020, setting out the core model that all importers and exporters will need to follow from January 2021 as well as the additional requirements for specific products such as live animals, plants, products of animal origin and high-risk food not of animal origin. We also provided important details of Member State requirements as traders and the border industry will need to ensure they are ready to comply with these, and not just Great Britain (GB) requirements. Indeed, as set out in the recently published ‘Reasonable Worst Case Scenario’ assumptions, it is largely the level of readiness for Member State requirements which will determine whether there is disruption to the flow of goods at the end of the transition period. This is why we have included additional signposting to those requirements throughout the document, and are encouraging all GB businesses not just to ensure their own readiness but also the readiness of EU businesses to whom they export, and throughout their supply chains.

Since July, the HMRC has worked closely with industry to further develop plans for the end of the transition period, and also to respond to industry questions since the publication of the first iteration of the Border Operating Model. This latest iteration of the Border Operating Model provides additional information in a number of key areas as set out below as well as clarifying a number of questions from industry.

Maintaining trade flows during the COVID-19 pandemic will be crucial in providing access to essential food and medical items and in limiting negative impacts on jobs and poverty.

The speed and scale of the crisis are unprecedented. But governments can ameliorate the impact. The following documents, hyperlinked to this page provide initial guidance for policymakers on best practices to mitigate pandemic-related trade risks, support trade facilitation and logistics, and implement trade policy in a time of crisis.

Managing Risk and Facilitating Trade in the COVID-19 Pandemic

Maintaining trade flows as much as possible during the COVID-19 pandemic will be crucial in providing access to essential food and medical items and in limiting negative impacts on jobs and poverty.

Some countries are closing border crossings and implementing protectionist measures such as restricting exports of critical medical supplies. Although these measures may in the short-term provide some immediate reduction in the spread of the disease, in the medium term they may undermine health protection, as countries lose access to essential products to fight the pandemic. Instead, governments should refrain from introducing new barriers to trade and consider removing import tariffs and other taxes at the border on critical medical equipment and products, including food, to support the health response.

Trade facilitation measures can contribute to the response to the crisis by expediting the movement, release, and clearance of goods, including goods in transit. The World Bank Group provides guidance and technical assistance to developing and least developed countries to implement best practices to facilitate the free flow of goods.

Do’s and Don’ts of Trade Policy in Response to COVID-19

Despite the initial inclination of policy makers to close borders, maintaining trade flows during the COVID-19 pandemic will be crucial. Trade in both goods and services will play a key role in overcoming the pandemic and limiting its impact in the following ways:

by providing access to essential medical goods (including material inputs for their production) and services to help contain the pandemic and treat those affected,

ensuring access to food throughout the world,

providing farmers with necessary inputs (seeds, fertilizers, pesticides, equipment, veterinary products)for the next harvest,

by supporting jobs and maintaining economic activity in the face of a global recession. Substantialdisruption to regional and global value chains will reduce employment and increase poverty.Trade policies will therefore be an essential instrument in the management of the crisis.

Trade policy reforms, such as tariff reductions, can contribute:

to reducing the cost and improving the availability of COVID-19 goods and services,

to reducing tax and administrative burdens on importers and exporters,

to reducing the cost of food and other products heavily consumed by the poor and contributing to themacro-economic measures introduced to limit the negative economic and social impact of the COVID-19 related downturn,

to supporting the eventual economic recovery and building resilience to future crises.

Governments with industries producing COVID-19 medical goods or food staples can further contribute by committing to refrain from limiting exports through bans or taxes. If export restrictions must be used, then they should be targeted, proportionate, transparent, and temporary.Measures to streamline trade procedures and facilitate trade at borders can contribute to the response to the crisis by expediting the movement, release, and clearance of goods, including goods in transit, and enabling exchange of services.

Reforms can be designed to reduce the need for close contact between traders, transporters and border officials so as to protect stakeholders and limit the spread of the virus, while maintaining essential assessments to ensure revenue, health and security. Interventions to sustain and enhance the efficiency of logistics operations may also be critical in avoiding substantial disruption to distribution networks and hence to regional and global value chains.

The covid-19 pandemic is increasingly a concern for developing countries. Using a new database on trade in covid-19 relevant products, this paper looks at the role of trade policy to address the looming health crisis in developing countries with highest numbers of recorded cases. It shows that export restrictions by leading producers could cause significant disruption in supplies and contribute to price increases. Tariffs and other restrictions to imports further impair the flow of critical products to developing countries.

Hong Kong customs has uncovered HK$85 million worth of smuggled cigarettes in the largest seizure of its kind in two decades, after authorities acted on intelligence indicating a syndicate was shipping the haul into the city in four containers.

Some 31 million cigarettes were stashed in the containers from Yokohama in Japan. They were then shipped through different ports in South Korea, Vietnam and mainland China, according to Lee Hoi-man, deputy head of the Revenue and General Investigation Bureau under customs.

He said the circuitous route was used by smugglers to avoid detection.

“The containers were shipped into three to four different ports before they came to Hong Kong,” Lee said adding that the contents listed on import documents were changed to throw off law enforcement in various jurisdictions.

Four men – one mainlander and three Hongkongers – aged between 24 and 41 were arrested in the operation on Monday. They were still being held for questioning on Tuesday evening.

Information on the containers was shared to a global database operated jointly by customs from different countries, under an anti-smuggling campaign code-named “Project Crocodile”.

A law enforcement source said the containers were left idle at another port since December, but were then suddenly moved across different countries before arriving in Hong Kong, one at a time since last Friday.

Lee said: “It is possible smugglers believed our frontline officers were tied up in dealing with the coronavirus outbreak.” He added that some of the contraband items were believed to be destined for countries in eastern Europe as some cigarette brands seized in the operation were popular there.

Hong Kong customs began investigating the syndicate in mid-December before identifying the four containers.

On Monday afternoon, officers from the Revenue and General Investigation Bureau swooped into action and seized 22 million sticks of cigarettes stashed in three containers at yards in Yuen Long, Sheung Shui and Man Kam To, arresting the four men.

At the Sheung Shui site, officers also seized 3,500 bottles of duty-not-paid liquor worth HK$2.5 million.

On Tuesday, the fourth container which had arrived from Shenzhen a day before was selected for inspection. Nine million cigarettes were found in it.

Lee said the combined haul had an estimated street value of HK$85 million, and was the biggest seizure of its kind in two decades in a single operation.

He said his team was working with overseas counterparts to determine the exact origin of the shipment and track down the ring leader and core syndicate members.

In Hong Kong, importing or exporting unmanifested cargo carries a maximum penalty of seven years in jail and a HK$2 million fine.

To mark International Customs Day 2020 – focusing on the theme of ‘fostering Sustainability for People, Prosperity and the Planet’, the following article from the Spring 2018 edition of World Trade Matters by Jan Hoffmann, the Chief of the Trade Logistics Branch, Division on Technology and Logistics at UNCTAD, is relevant. The article discusses global trade facilitation reforms, the digitalisation of trade and measures towards ensuring long-term sustainability in the maritime industry.

Confronted with growing populism and a surge in protectionist measures recorded by the WTO, policy makers and enterprises are struggling to avoid a backlash in international trade. At UNCTAD’s Trade Logistics Branch, we support these endeavours by helping to make trade work better. Through trade facilitation reforms, the promotion of digitalisation, and ensuring the long-term sustainability of international transport, we aim at ensuring that the international movement of goods is not confronted with unnecessary obstacles and costs.

A multilateral agreement to facilitate international trade

Under the Trade Facilitation Agreement (TFA) of the World Trade Organization (WTO), developing countries commit to implement a number of very practical measures that make trade easier and more transparent. Countries are obliged to publish duties and procedures on the web, traders can transmit their declarations prior to the arrival of the goods, payments can be made electronically, and fees and charges must not become hidden taxes to generate income for the government. These are but some of the 37 concrete measures grouped into 12 Articles of the TFA. They are all useful and help make trade more efficient.

However, many of these measures involve an initial investment or reforms that require human and financial resources to start with, which developing countries many not have. The good news is that the TFA also includes a novel mechanism – the so called “Special and Differential Treatment” – that helps developing countries plan and acquire the necessary capacity prior to being fully committed to comply with all 12 Articles. Concretely, the mechanism puts the developing countries in the position – and obligation – to analyse and notify their own implementation capacity. At UNCTAD, we are working closely with the developing countries to enable them to do so. Our main counterpart in this endeavour are the National Trade Facilitation Committees (NTFCs) that each country must set up under the TFA. UNCTAD’s Empowerment Programme for NTFCs includes training and knowledge development for the members of the NTFC, combined with advisory services and the development of a Roadmap of TFA implementation.

By the same token, UNCTAD also supports developing countries in setting up Trade Information Portals. Under the TFA, members of the WTO are obliged to make relevant information on tariffs and trade procedures available on-line. UNCTAD’s Trade Information Portals not only help countries become compliant with this obligation, but in the process of analysing and publishing applicable trade procedures, a Trade Information Portal effectively helps countries identify the potential for the further simplification of procedures. Thanks to these new insights, NTFCs can then develop programmes and reforms that subsequently ensure the further simplification of procedures.

Technological progress will never be as slow as today

My favourite provision of the TFA is Article 10.1., as it provides for a dynamic dimension of the Agreement. According to this article, countries need to minimize “the incidence and complexity of import, export, and transit formalities”, continuously “review” requirements, keep “reducing the time and cost of compliance for traders and operators”, and always choose “the least trade restrictive measure”. As such, even if a country is compliant with all TFA provisions today, countries will need to continue monitoring if existing procedures are still appropriate in view of technological or regulatory developments.

As trade becomes increasingly digitalised, and new technologies which do not yet exist will be developed, it will be important that governments continuously revise and review the applicable rules and regulations.

Digitalisation comes in stages. First, we optimize existing procedures, making use of cargo tracking, the Internet of Things, blockchain et al. Second, new businesses are developed which could not exist without the new technologies; new platforms come into being and we see more “uberisation”. Finally, there is transformation and science fiction; still in our lifetime Artificial Intelligence will overtake human capabilities to manage international trade and its logistics.

But let us take one step at a time. At UNCTAD, we support developing countries through eTrade readiness assessments, the development and upgrade of technological solutions in Customs automation and Single Windows, and by providing a Forum for our members to analyse and discuss the challenges that come with digitalisation. We encourage the development of global standards that allow for interoperability among new systems. The challenge for policy makers it to encourage private sector investments in new technologies and solutions, while ensuring that no new monopolies emerge that might exclude smaller players.

And it has to be sustainable

While we aim at ensuring continued growth in international trade, there is a catch. The transport of this trade encompasses increasing externalities, such as pollution, green-house-gas emissions, and congestion.

Ports need to minimise social and environmental externalities. Many port cities are among the most polluted places to live, as ships burn heavy oil, and delivering trucks produce noise and cause traffic congestions. In addition, ports need to be resilient in the face of disruptions and damages caused by natural disasters and climate change impacts.

International transport, including shipping, needs to play a larger role in addressing global warming and contribute to mitigating the carbon emissions that are causing climate change. Shipping emits less carbon dioxide (CO2) per ton-mile than other modes of transport, but then due to its sheer volume it also produces many ton-miles. Would it be possible that the industry could be charged by its main regulatory body not per ship tonnage (as is currently the case), but per tonne of CO2 emission?

Currently, the International Maritime Organization is funded proportional to the tonnage registered under the members’ flags. Like this, Panama, Marshall Islands and Liberia pay for the largest share of the IMO budget – and in the end, this is passed on to the ship-owner, who in turn passes this on to the shipper, who will charge the consumer. This is a good established mechanism that could be expanded to also internalize the external costs of CO2 emissions.

Being the most globalized of all businesses, maritime transport should consider adopting a global regime that helps further internalize its environmental externalities – to ensure prosperity for all.

It is all about efficiency

Investing in trade facilitation reforms, making intelligent use of the latest technologies, and ensuring that externalities are internalized are all several sides of the same coin. Trade efficiency is necessary to promote an open international trading system. It requires a continuous effort by policy makers to continuously review current procedures, apply the most appropriate technological solutions, and support an efficient allocation of scarce resources.

Source: Jan Hoffman, UNCTAD – originally published in World Trade Matters, Spring Edition, 2018

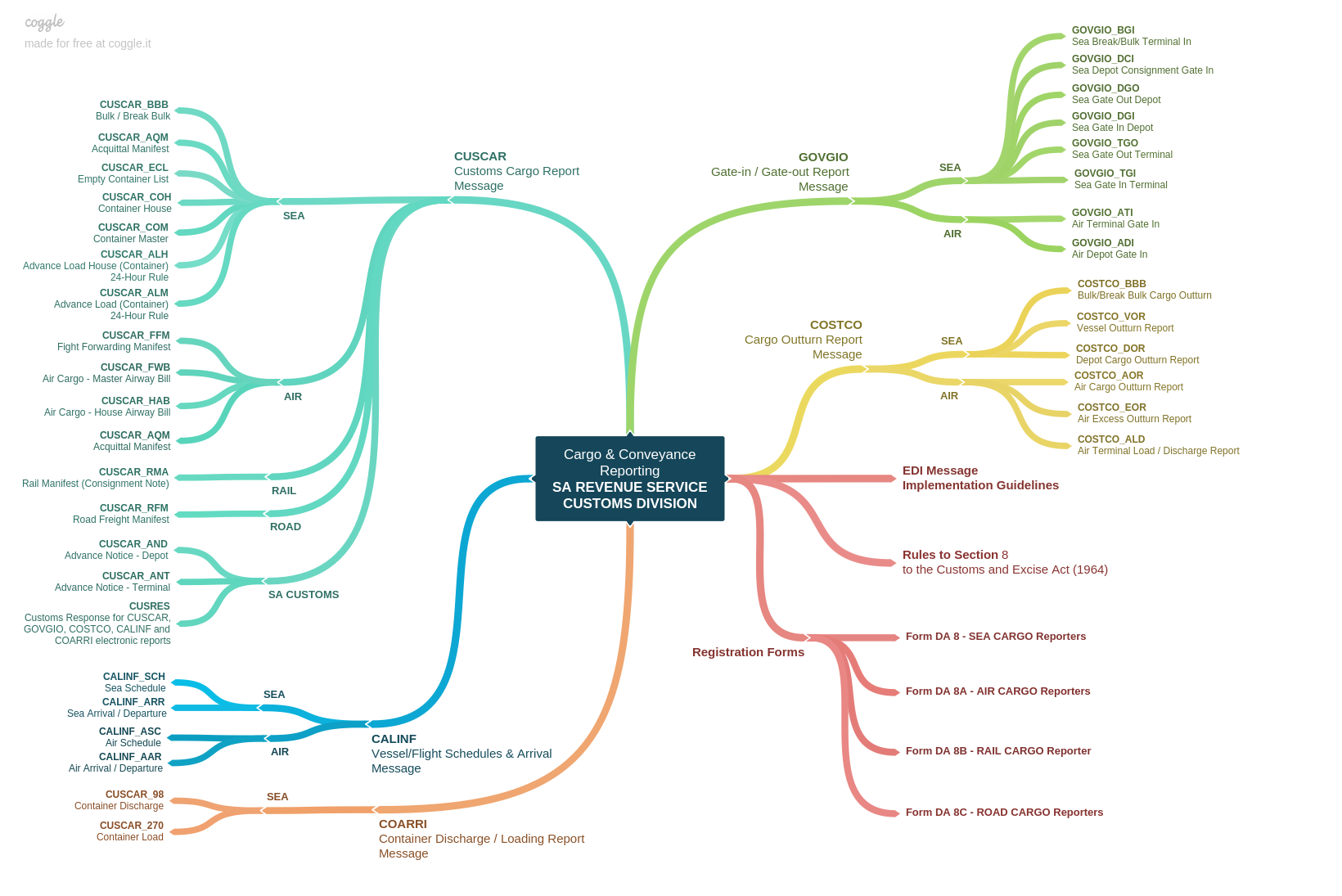

This Friday, 20 April 2018, SARS Customs will implement its new Cargo, Conveyance and Goods Accounting solution – otherwise known as the Cargo Processing System (CPS). In recent years SARS has introduced several e-initiatives to bolster cargo reporting in support its electronic Customs Clearance Processing System (iCBS), introduced in August 2013.

Followers of SARS’ New Customs Acts Programme (NCAP) will recognise that the CPS forms part of one of the three core pillars of the new legislative programme, better known as Reporting of Conveyances and Goods (RCG). The other two pillars are, Registration, Licensing and Accreditation (RLA) and Declaration Processing (DPR). More about these in future articles. In order to expedite the implementation of the new Acts, SARS deemed it necessary to introduce elements of the new functionality via a transitional manner under the current Customs and Excise (1964) Act.

Proper revenue accounting and goods statistical reporting, can only be adequately achieved if Customs knows what goods ‘actually’ arrive, transit and exit it’s borders. Many countries, since the era of heightened security (post 9/11), have invested heavily in the re-engineering of policies and systems to address the threat of terrorism. This lead to a re-focus of resources and energies to develop risk management systems based on ‘advanced information’. SARS has invested significantly in automated systems in the last decade. Shortly, SARS it will also introduce a new automated risk engine with enhanced capabilities to include post clearance audit activities.

It should also not come as a surprise to anyone conversant with Customs practice, that international Customs standards such as the WCO’s SAFE Framework of Standards, the RKC and the Data Model are prevalent in the new Customs legal dispensation and its operational business systems.

South Africa will now follow several of its trading partners with the introduction of ‘advance reporting of containerised cargo’ destined for South African sea ports. This reporting requires carriers and forwarders to submit ‘advance loading notices’ to SARS Customs at both master and house bill of lading levels, 24 hours prior to vessel departure.

The implementation of CPS is significant in terms of its scope. It comprises some 30 odd electronic cargo notices and reports across the sea, air, rail and road modalities. These reports form the ‘pipeline’ of information deemed necessary to ensure that the ‘chain of custody’ is visible and secure from point of departure to final destination. For the first time, South Africa will also require cargo reporting in the export domain.

It is no understatement that the CPS initiative is a challenge in particular to new supply chain entities who have not been required in the past to submit electronic reports. In order to meet these reporting requirements, a significant investment in systems development and training is required on the part of SARS and external trade participants. To this end, SARS intends to focus on ramping up compliance amongst all cargo reporters across all transport modalities. The first modality will be road, which is the most significantly developed and supported modality by trade since the inception of manifest reporting under the Customs Modernisation Programme. The remaining transport modalities will receive attention once road is stabilised.

This edition of WCO News features a special dossier on the theme chosen by the WCO for 2018, namely “A secure business environment for economic development”, with articles presenting initiatives and related projects that contribute to creating such an environment. The articles touch on authorized economic operators, national committees on trade facilitation, coordinated border management, performance measurement, e-commerce, data analysis, and partnerships with the private sector.

For sub-Saharan African readers, look out for the write up of the Customs systems interconnectivity and the challenges and opportunities for Customs administrations in the SACU region.

Other highlights include articles on Customs systems interconnectivity in the Southern African Customs Union, on the experience of a young Nigerian Customs officer who participated in the Strategic Management and Intellectual Property Rights Programme at Tokyo’s Aoyama Gakuin University, on how the WCO West and Central Africa region is using data to monitor Customs modernization in the region, and on the benefits that can be derived by facilitating transit procedures.

The Indian Customs department (CBEC) has allowed self-sealing procedure as of 1 October for containers to be exported, as it aims to move towards a ‘trust based compliance environment’ and trade facilitation for exporters.

In a circular to all Principal Chief Commissioners, the Central Board of Excise and Customs (CBEC) said exporters who were availing facility of sealing at the factory premises under the supervision of customs authorities will be automatically entitled for self-sealing facility.

It said that permission once granted for self-sealing at an approved premise will remain valid unless withdrawn. However, in case of change in the premise, a fresh approval from Customs department will be required.

“The new self-sealing procedure shall come into effect from October 1, 2017. Till then the existing procedure shall continue,” the CBEC said.

It asked field officers to notify a Superintendent-rank officer to act as the nodal officer for the self-sealing procedure.

The officer will be responsible for coordination of the arrangements for installation of reader-scanners.

Earlier in July, the CBEC had said it will introduce the system of self-sealing by 1 September , as against the practise of sealing of containers under the supervision of revenue officials.

However, the CBEC now said that exporters can self-seal containers using the tamper proof electronic seals from 1 October 2017.

Under the new procedure, the exporter will have to declare the physical serial number of the e-seal at the time of filing the online integrated shipping bill or in the case of manual shipping bill before the container is dispatched for the port.

The exporters will directly procure RFID seals from vendors.

“In case, the RFID seals of the containers are found to be tampered with, then mandatory examination would be carried out by the Customs authorities,” the CBEC said.

From October 1, the exporters will need to furnish e-seal number, date of sealing, time of sealing, destination customs station for export, container number and trailer track number to the customs authorities.

In a circular in July, the CBEC had said it endeavours to create a trust based environment where compliance with laws is ensured by strengthening risk management system and Intelligence setup of the department.

Accordingly, CBEC has decided to lay down a simplified procedure for stuffing and sealing of export goods in containers. Source: The India Times > Economic Times, 5 September 2017.

Historically, a customs officer’s “intuition” backed up by his/her knowledge and experience served as the means for effective risk management. In the old days (20 years ago and back) there wasn’t any need for all this ‘Big Data’ mumbo jumbo as the customs officer learnt his/her skill through painful, but real-life experience, often under bad and inhospitable conditions.

Today we are a lot more softer. The age of technology has superseded, rightly or wrongly, the human brain. Nonetheless, governments thrive on their big-spend technology budgets to ensure the safety of their economies and supply chains.

No less, the big multinational corporations whose ‘in-house’ business is no longer confined by national boundaries or continents are responsible for the generation of huge amounts of data which need to extend to the limits of their operations. When the products of such business are required to traverse national boundaries and continents, their logistics and transport intermediaries, financiers, and insurers become themselves tied up in the vicious cycle of data generation and transfer, also spanning national boundaries to ensure those products arrive at their intended destinations – intact, in time and fit for purpose. Hence we have what as become known as the international supply chain.

It does not end there. Besides the Customs authorities, what about the myriad of other government regulatory authorities who themselves have a plethora of forms and information requirements which must be administered and approved prior to departure and upon arrival of goods at their destination.

Inefficiencies along the supply chain culminate in delays with added cost which dictates the viability for sale and use of the product during delivery. These may constitute what is called non-tariff barriers (or NTBs) which negatively impact the suppliers credibility in international trade.

The bulk of this information is nowadays digitised in some for or other. It is obviously not all standardised and structured which makes it difficult to align, compare or assimilate. For Customs it poses a significant opportunity to tap into and utilise for verification or risk management purposes.

The term ‘Big Data’ embraces a broad category of data or datasets that, in order to be fully exploited, require advanced technologies to be used in parallel. Many big data applications have the potential to optimize organizations’ performance, (and here we have it) the optimal allocation of human or financial resources in a manner that maximizes outputs.

The purpose of this paper is to discuss the implications of the aforementioned big data for Customs, particularly in terms of risk management. To ensure that better informed and smarter decisions are taken, some Customs administrations have already embarked on big data initiatives, leveraging the power of analytics, ensuring the quality of data (regarding cargos, shipments and conveyances), and widening the scope of data they could use for analytical purposes. This paper illustrates these initiatives based on the information shared by five Customs administrations: Canada Border Services Agency (CBSA); Customs and Excise Department, Hong Kong, China (‘Hong Kong China Customs); New Zealand Customs Service (‘New Zealand Customs’); Her Majesty’s Revenue and Customs (HMRC), the United Kingdom; and U.S. Customs and Border Protection (USCBP). Source: WCO

The WCO Policy Commission, held in Moscow, Russian Federation, from 5 to 7 December 2016 under the chairmanship of Mr. R. Davydov, brought to the fore the key role of Customs in creating a sustainable and efficient e-commerce ecosystem, reviving-up the exchange of data between stakeholders and enhancing risk-management through electronic interface. The other main topics discussed during the Commission pertained to trade facilitation, security, the enhancement of the Customs/Tax cooperation and the modernization of Customs administrations.

The newly established WCO Working Group on E-Commerce will work to tackle the different dimensions of e-commerce by collecting and exchanging best practices in the field, stocktaking and leveraging some of the ongoing work being carried out by other entities and drawing up proposals geared towards the development of practical solutions for the clearance of e-commerce shipments, including appropriate duty/tax collection mechanisms and control procedures.

Concerning the in-depth discussions on Custom /Tax cooperation, the WCO issued this year “Guidelines for strengthening cooperation and the exchange of information between Customs and Tax authorities at the national level” and will continue working on topics of common interest for Customs and Tax experts such as transfer pricing, drawback and Illicit Financial Flows (IFF).

During the Commission, WCO Secretary General Kunio Mikuriya, confirmed the WCO Theme for 2017 “Data Analysis for Effective Border Management” and stressed the impact of the digital revolution and the need to address promptly the challenges posed to the global economy. The Secretary General invited all the WCO Members to promote and share information in the coming months on how they are leveraging the potential of data to advance and achieve their objectives and respond to the expectations of traders, transport and logistic operators, and governments.

As data analysis will be emphasized in 2017 as a force multiplier for Customs administrations, it is relevant to highlight that the WCO is carrying out a Study to collect best practices among its members to assess and promote initiatives in the area of e-commerce. A previous analysis of preliminary data underscored the need for digitalization of processes, better sharing of information between e-commerce stakeholders and customs for improved risk management and the necessity for harmonization in the low-value shipment processes. Source: WCO

The Indian Customs department (CBEC) has allowed self-sealing procedure as of 1 October for containers to be exported, as it aims to move towards a ‘trust based compliance environment’ and trade facilitation for exporters.

The Indian Customs department (CBEC) has allowed self-sealing procedure as of 1 October for containers to be exported, as it aims to move towards a ‘trust based compliance environment’ and trade facilitation for exporters.

You must be logged in to post a comment.