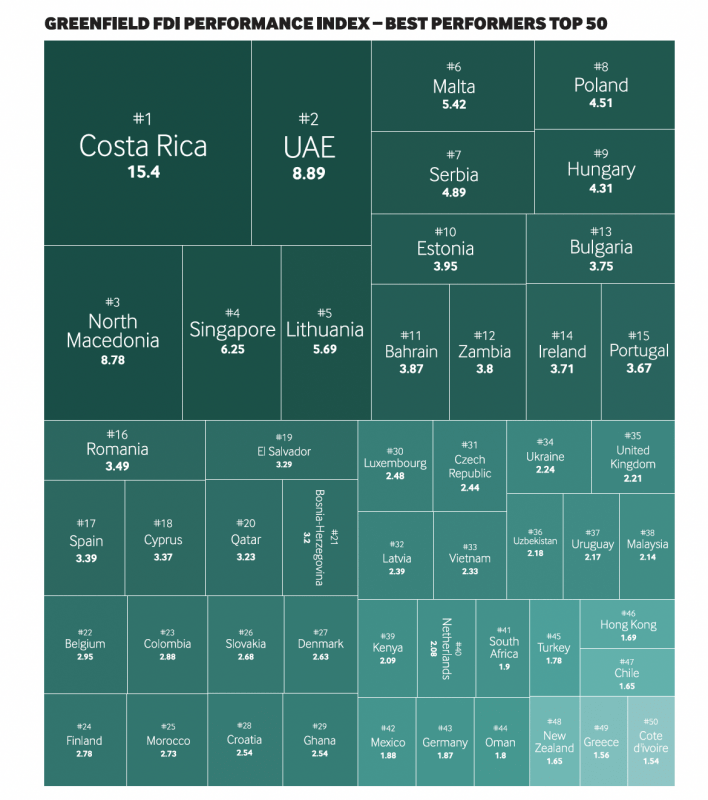

According to the seventh edition of the Greenfield FDI Performance Index, Costa Rica has entrenched its global leadership as the country that attracts the most foreign direct investment (FDI) relative to the size of its economy, thus proving the resilience of its investment proposition in the wake of the Covid-19 pandemic. The UAE and North Macedonia also showed their strength, coming in second and third respectively.

The pandemic redrew the map of the world’s best FDI outperformers relative to the size of their global gross domestic product (GDP). In this respect, Costa Rica is both an outperformer and an outlier as the only Latin American country in the top 10, which is dominated by major business hubs such as the UAE and Singapore, and countries in emerging Europe. On the other hand, African countries paid the highest price as investment flew back to the safety of OECD countries. In 2019, as many as five African countries featured in the top 10; two years later, none of them made it.

Of the 84 countries recording more than 10 FDI projects in 2021 and thus being considered for the 2021 index, 68 have an index score greater than 1.0, indicating a larger share of investment projects relative to its share of GDP. The remaining 16 have a score less than 1.0, indicating a smaller share of projects relative to GDP.

Costa Rica’s 2021 score stands at 15.5. This suggests that, given the size of its economy, it attracts 15.5 times more projects than the size of its GDP would suggest.

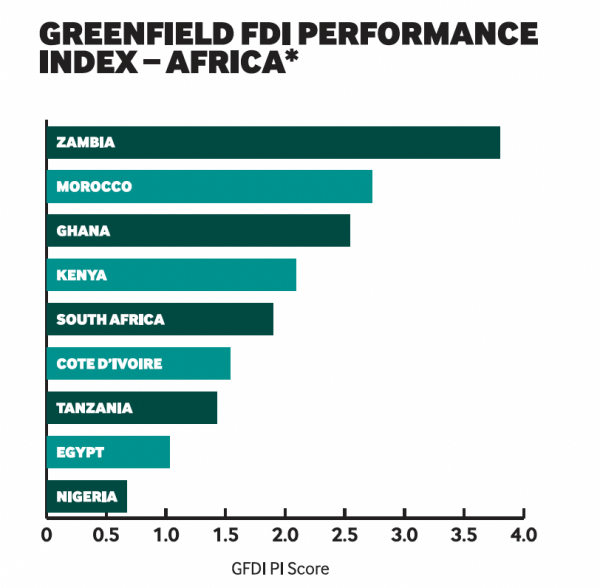

The 2021 index contains nine African countries, and continues a trend that has seen African nations appear less in the index compared to the previous edition – only countries with 10 or more FDI projects in the full year are considered. Of those included, only Egypt (1.0) and Tanzania (1.4) saw their scores increase from 2020.

South Africa had an unfortunate year in that while FDI increased, its economic growth outpaced investment, resulting in a drop in this year’s index.

In a meeting with prospect investors, Jamaican industry minister Aubyn Hill eloquently conveyed his vision for a new free zone in Caymanas, Kingston. A smirk appeared on his face as he delivered the final line.

“Developers will enjoy a 50-year total exemption on corporate income tax,” Mr Hill said on June 16, seemingly indifferent to the 15% global minimum tax rate that 136 countries, including Jamaica, are expected to implement from 2023 onwards.

His remarks embody the ambiguity of many developing countries towards the OECD-sponsored reform. While most of them subscribe to the idea behind the reform, they cannot help seeing fiscal incentives as a key pillar of their investment promotion strategies.

Viable tool

Policy-makers across the globe have resorted to tax cuts to lure foreign businesses as competition for investment went global in the past 40 years. The world’s weighted average statutory corporate income tax (CIT) rate has declined from 46.5% in 1980 to 25.4% in 2021, according to figures from the Tax Foundation.

Developing countries in particular have raced to lower national CIT rates to boost their investment appeal. The global minimum tax reform now puts them between a rock and a hard place.

“From a resource mobilisation perspective typical of a finance minister, the reform may be seen as a good base to stop the race to the bottom,” Bogolo Joy Kenewendo, an economist and former minister of investment of Botswana, tells fDi, on the sidelines of AICE2022, the annual gathering of free zones organised by the World Free Zones Organisation in Jamaica in June 13-17.

“However, from an investment promotion perspective, tax incentives are the tools we use to attract investment. OECD countries, in particular G20 countries, have already gone through that development phase and built their industries. They no longer need that race to the bottom, but what about countries that see this as a viable tool?”

The OECD proposal is built on two main pillars. The first proposes to re-allocate some taxing rights over multinational enterprises from their home countries to the markets where they have business activities and earn profits, regardless of whether firms have a physical presence there. The second introduces a global minimum corporate tax rate set at 15%, which will apply to companies with revenue above €750m and is estimated to generate around $150bn in additional global tax revenues annually.

Free zones

Developing countries often resort to fiscal incentives to offset structural weaknesses that would otherwise sink their hopes of landing big ticket investments. Free zones are a case in point. They have flourished on their unique combination of fiscal incentives, customs facilitations and plug-and-play infrastructure. Unctad tracked as many as 5383 free zones in 2019, 89% of which were located in developing economies.

Almost 80% of the special economic zone (SEZ) laws worldwide provide for fiscal incentives, such as tax holidays for a defined period of often five to 10 years, or the application of a reduced tax rate, Unctad also found.

“Differentiated taxes are a necessary compensatory measure to offset the inherent inefficiencies and disadvantages of developing nations which suffer from high energy costs, deficient infrastructure, and higher inbound/outbound transportation costs,” Cesare Zingone, the CEO of Zeta Group Real Estate, a developer of free zones in Central America, tells fDi.

“Therefore an equal minimum tax would increase compliance costs, place developing countries at a competitive disadvantage, and finally favour the relocation of companies to wealthy, developed nations. However if the minimum global tax were to be implemented, it would be imperative for developing countries to implement other compensatory measures, such as reducing social security costs on labour, property taxes or import duties.”

Regardless of the OECD’s global minimum tax push, fiscal incentives continue to feature at the heart of the offer of some of the world’s biggest free zones under development. Among others, in Guatemala, developer Pacific Investment is developing 1200 hectares of land for the new Michatoya SEZ, which promises no CIT for 10 years; Indonesia has just named the island of Natuna Regency in the South China Sea as a SEZ, offering zero CIT for 10 years; Iraq is launching three SEZs to trigger development, also offering zero CIT for the duration of the project.

If policy-makers and zones developers seem unfazed by the global minimum tax reform, the OECD is equally unfazed.

“SEZs don’t seem to have done much to prepare for this. The reality is that this is happening, and they will have to get ready for this to come,” Pascal Saint-Amans tells fDi, oozing his confidence in the fact that once the EU and US approve the reform, a domino effect will prompt all the countries that endorsed the reform to fall in line.

However, the road for the OECD remains uphill. In the EU, Hungary has vetoed a key vote on June 17 to approve the reform.

Back in Caymanas, Mr Hill continued to mingle with prospect investors, pushing the CIT exemption as the icing on the cake for the package on offer. As with any other policy-maker in developing economies, he is taking his chances at the policy-making table — and so is the OECD.

The trend of declining foreign direct investment (FDI) to Africa is set to exacerbate significantly in 2020 amid the dual shock of the coronavirus pandemic and low prices of commodities, especially oil.

FDI flows to the continent are forecast to contract between 25% and 40% based on gross domestic product (GDP) growth projections as well as a range of investment specific factors, according to UNCTAD’s World Investment Report 2020.

“Although all industries are set to be affected, several services industries including aviation, hospitality, tourism and leisure are hit hard, a trend likely to persist for some time in the future,” said UNCTAD’s director of investment and enterprise, James Zhan.

Manufacturing industries intensive in global value chains are also strongly affected, a sign of concern for efforts to promote economic diversification and industrialization in Africa.

Overall, there is a strong downward trend in the first quarter of 2020 for announced greenfield investment projects, although the value of projects (-58%) has dropped more severely than their number (-23%).

Similarly, as of April 2020, the number of cross-border merger and acquisition (M&A) projects targeting Africa had declined 72% from the monthly average of 2019.

Hope for recovery

However, two distinct factors offer hope for the recovery of investment flows to the continent in the medium to long run. The first is the higher value being assigned to ties to the continent by major global economies, promoting investment in infrastructure, resources, but also industrial development.

Investments from these countries, which have varying degrees of political backing, despite being affected by the joint impact of COVID-19 and low commodity prices to some degree, could be relatively more resilient.

The second is deepening regional integration due to the commencement of trade under the African Continental Free Trade Area (AfCFTA) after years of deliberation and the expected finalization of its investment protocol.

In the short term, curtailing the extent of the investment downturn and limiting the economic and human costs of the pandemic is of paramount importance.

Longer term, diversifying investment flows to Africa and harnessing them for structural transformation remains a key objective. Both of these objectives will require a prudent, coordinated and timely response from countries on the continent.

FDI was already on the decline before the crisis

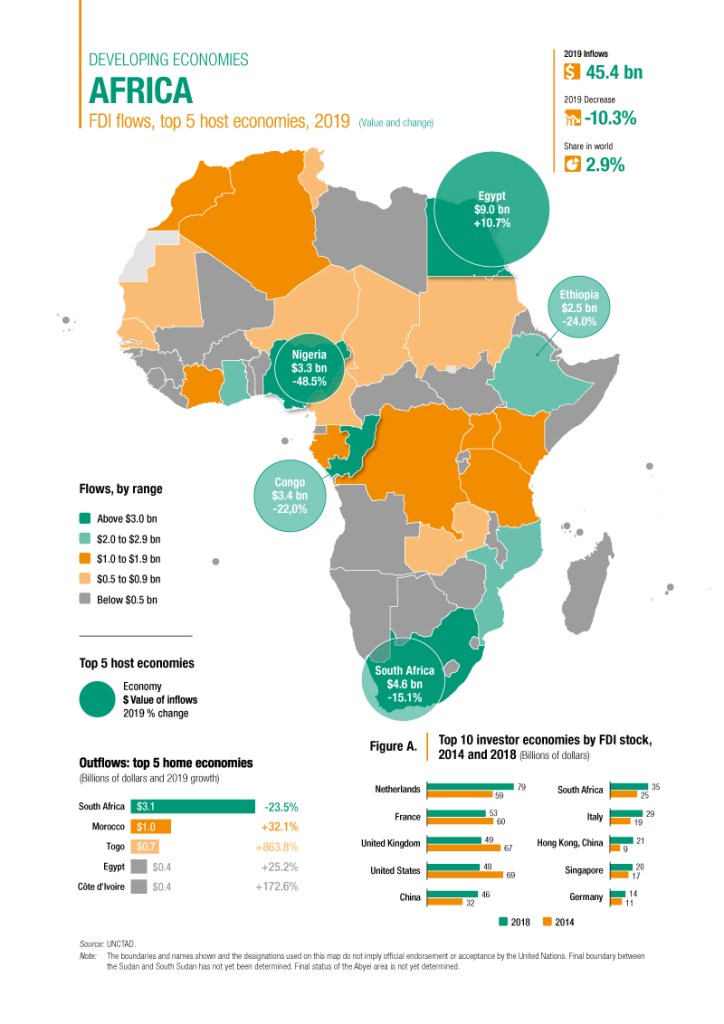

The COVID-19 crisis has arrived at a time when FDI was already in decline, with the continent having experienced a 10% drop in inflows in 2019 to $45 billion.

The negative effects of tepid global and regional GDP growth and dampened demand for commodities inhibited flows to countries with both diversified and natural resource-oriented investment profiles alike, although a few countries received higher inflows from large new projects.

North Africa

FDI inflows to North Africa decreased by 11% to $14 billion, with reduced inflows in all countries except Egypt, which remained the largest FDI recipient in Africa in 2019, with inflows increasing by 11% to $9 billion.

Sub-Saharan and Southern Africa

After a significant increase in 2018, FDI flows to Sub-Saharan Africa decreased by 10% in 2019 to $32 billion.

Southern Africa was the only sub-region to have received higher inflows in 2019 (22% increase to $4.4 billion) but only due to the slowdown in net divestment from Angola.

FDI inflows to South Africa decreased by 15% to $4.6 billion in 2019, despite key investments in mining, manufacturing (automobiles, consumer goods) and services (finance and banking).

West Africa

FDI to West Africa decreased by 21% to $11 billion in 2019. This was largely driven by the steep decline in investment in Nigeria due to new investment regulations for multinational enterprises in the oil and gas industry.

East Africa

FDI flows to East Africa also decreased, by 9% to $7.8 billion. Inflows to Ethiopia contracted by a fourth to $2.5 billion caused to some degree by political tensions in parts of the country.

Similarly, inflows to Kenya dropped by 18% to $1.3 billion despite several new projects in IT and healthcare.

Central Africa

Central Africa received $8.7 billion in FDI, marking a decline of 7%. The key highlight in the sub-region was the decrease in flows to the Democratic Republic of the Congo (9% to $1.5 billion).

The Netherlands overtook France as the largest investor by stock

On the basis of FDI stock data through 2018, the Netherlands overtook France as the largest foreign investor in Africa.

The investment stock held by the United States and France in Africa declined by 15% and 5% respectively, owing to profit repatriation and divestment. Meanwhile, the investment stock of the United Kingdom and China increased by 10% each.

FDI outflows also fell in 2019, by approximately a third

FDI outflows from Africa decreased by 35% to $5.3 billion. South Africa continued to be the largest outward investor despite the reduction in outflows from $4.1 billion to $3.1 billion.

Outflows from Togo increased significantly, from a mere $70 million to $700 million, a tenfold increase. In North Africa, Morocco also increased outward FDI, to approximately $1 billion from $800 million in 2019.

Source: UNCTAD, World Investment Report, 16 June 2020

Recently while reading of Transnet’s terminal capex expansion plans, I came across this interesting if not highly improbable plan featured in an article by Harry Valentine on Maritime Executive. I say improbable given the current economic and labour situation prevailing in South Africa at this time, not to mention the fact that the Transnet controlled Port of Ngqura is considered South Africa’s transhipment hub. Nonetheless, I think its admirable that such ideas are conceived and with a bit of thought and application are presented for consideration. From a Customs’ perspective such plans – in particular the notion of a floating terminal – could pose some interesting challenges (err opportunities) for SARS particularly given impending new compliance, licensing and reporting requirements contained in the new Customs Control Act.

The Port of Los Angeles has welcomed its first 18,000-TEU ultra-large container ship, and Brazil, with a population almost as large as the U.S. and with future prospects of increased trade with Asia, could see such ships arriving via South Africa.

The projected future volume of container traffic that will pass through Brazilian ports would warrant future operation of ultra-large container ships between Brazil and major Asian transshipment terminals. However, it would take much investment and likely many years before a Brazilian port and terminal would be able to berth and service these vessels. One option would be to develop a transshipment port in South Africa that could serve as a terminal for ultra-large container ships that sail from such ports as Busan, Inchon, Shanghai and Hong Kong carrying containers destined for South America.

South Africa offers two bays capable of accepting ultra-large container ships. Richards Bay in the Northeast offers a draft clearance of 19 meters, while Saldanha Bay just north of Cape Town offers a draft of 21 meters. Bulk and ore freight terminals operate at both locations. Saldanha Bay is larger than Richard’s Bay, located near the large City of Cape Town and is closer to the shipping lane between South America and the Far East. It is also close to St. Helena Bay where waiting vessels may drop anchor.

When Richards Bay is at capacity, alternative areas where waiting vessels may drop anchor with a measure of protection from stormy seas are located at much greater distances. The Port of Durban is still Africa’s busiest container port and regularly operates at near-capacity. However, Durban and companion ports at Maputo, Port Elizabeth, Coega, East London and Cape Town have insufficient depth to accommodate ultra-large container ships. Saldanha Bay is a natural inlet that offers the necessary depth and has available space to develop a transshipment terminal to the south of the ore terminal.

There are tentative plans to borrow a precedent from Egypt and anchor a floating LNG storage tanker in Saldanha Bay, perhaps near the southern end of the inlet, to serve a variety of customer requirements. Tanker vessels could regularly carry LNG from Mozambique, Tanzania and Angola to the floating storage terminal. Operational precedents established at the Port of Durban could ensure smooth operation of maritime vessels entering and leaving Saldanha Bay, especially with excess vessels being able to drop anchor in St. Helena Bay as well as nearby Table Bay at Cape Town some 60 nautical miles away.

Future ultra-large container ships of 22,000 TEUs would offer savings in terms of average cost per container on the segment between Saldanha Bay and distant East Asian ports at or near the South China Sea. Automated terminal operations that include transfer of containers among vessels could contribute to competitive transportation costs to a variety of destinations along South America’s Atlantic coast as well as several South African ports, perhaps extending as far north as Nigeria on the Atlantic Coast (Asia – Africa trade), Tanzania on the East Coast (Africa – South America trade), as well as domestic Africa -Africa trade.

While South Africa’s economy may presently be under-performing, South African authorities have the option of inviting foreign investors and developers to explore the option of developing a transshipment super port at Saldanha Bay. Future trade through Saldanha Bay would include containers sailing to and from East Asian transshipment terminals such as Port of Colombo and Port of Singapore to connect into the combination of West Coast Africa – Asia and Atlantic Coast South America -Asia trade. Such combined trade enhances prospects for potentially viable transshipment port and terminal operations at a South African bay.

A transshipment super port at the southern end of the African continent would mostly transfer containers that originate from and be destined for foreign ports. Only a minority of the containers would originate from or be destined for domestic South African ports. South African exporters and importers would benefit from lower transportation costs per container compared to the transportation costs per container aboard smaller vessels.

It’s an idea worth considering.

Floating Islands

Cape Town is at the crossroads of ships that carry the trade between Asian nations and nations along the Atlantic Coast of South America and sub-Sahara West Africa. There may be future scope for an offshore, floating transshipment terminal built at Saldanha Bay and assembled either at Cape Town or St Helena Bay to reduce per-container transportation costs along this trade route. Such a terminal would attract interest from overseas. A floating hotel partially surrounded by breakwaters and permanently anchored offshore near a coastal city could be connected to the mainland using floating bridges and water taxi service.

There may be scope to expand upon the technology to develop multiple floating structures in a calm water area, with bridges connecting between them at strategic locations to maintain navigable canals between them. While water taxis could shuttle visitors between mainland and an offshore floating island, semi-floating bridges could also connect between mainland and such islands that may include business districts and even residential areas.

Coupled floating structures may also serve as an airport with a runway for commuter size of aircraft and perhaps even comparable size of wing-in-ground effect vehicles that provide service between coastal cities.

South Africa is moving away from a policy promoting trade and investment to one that contradicts this, a roundtable on SA-European Union (EU) trade relations heard on Tuesday.

This comes as global foreign direct investment (FDI) flows jumped 36% last year to their highest level since the global economic and financial crisis began in late 2008, but plummeted in emerging markets, especially SA.

The most recent United Nations (UN) Conference on Trade and Development global investment trends monitor shows FDI into SA fell 74% to $1.5bn last year, while FDI inflows to Africa fell 31% to about $38bn.

Central Africa and Southern Africa saw the largest declines in FDI. The end of the commodity “supercycle” and the plunge in oil prices affected new project developments drastically, the UN body said. This had also affected Brazil, Russia and China, but not India, whose economy had surged ahead of late.

Peter Draper, MD of Tutwa Consulting, which researches policy and regulatory matters in emerging markets, said the promulgation of legislation such as the private security bill and the expropriation bill, created an impression that SA was not an attractive investment destination.

“What lies behind all of that, I think, is an ideological agenda, which is not favourable to business,” he said. “Geopolitically there is no love between SA and the US and SA and the EU. (But) There is lots of love for the Brics (Brazil, Russia, India, China, SA).”

South African and international business have raised the alarm over the quiet signing into law of SA’s Promotion and Protection of Investment Bill late last year, after the government had acknowledged that it would do little to promote trade.

Meanwhile, the Department of Trade and Industry said last week that the African National Congress had directed its economic transformation subcommittee to review the trade agreements signed by SA since 1999.

It said SA’s goal in “negotiating” trade agreements was to support national development objectives, promote intra-African trade and the integration of SA into global markets. This is likely to be highly controversial after the government from 2013 unilaterally cancelled about 13 bilateral investment treaties with major EU countries, drawing warnings from the bloc that this could damage trade relations.

Investors fear the Protection of Investment Bill has diluted recourse to international arbitration over trade disputes, and enhances the possibility of expropriation. Critics also say it contradicts SA’s obligations under the Southern African Development Community’s finance and investment protocol, by undermining equitable treatment between foreign and domestic investors.

John Purchase, CE of agribusiness association Agbiz, which with Tutwa Consulting organised yesterday’s roundtable, said the bill had not answered “all those questions around the bilateral investment treaties”. Source: Business Day

fDi Markets that even without the data for December, it is already clear that Kenya enjoyed a major increase in inward investment in 2015 when compared with 2014.

Greenfield investment monitor fDi Markets has tracked a bumper year for Kenya-destined FDI. Excluding retail, the monitor has recorded 78 projects between January and November 2015, a 36.84% increase compared with the whole of 2014. FDI entering Kenya during the 11 months of 2015 (for which data is available) has already surpassed that recorded for 2013, the previous multi-year high. fDi Markets is set to record 2015 as witnessing the highest number of inward FDI projects for Kenya since the it commenced tracking data in 2003.

fDi Markets has tracked the upward trend as beginning in 2007, with FDI levels increasing year on year between then and 2011. In the period between 2011 and 2014 a period of consolidation occurred in which inward investment fluctuated, with decreases recorded in 2012 and 2014. Between 2007 and 2015, fDi Markets has tracked a 766.66% increase in project numbers and a total capital investment of $14.04bn.

Kenya’s FDI resurgence in 2015 is further illustrated when compared with the rest of Africa. During 2015, Kenya attracted 12.58% of all FDI entering Africa, with only South Africa, a long-time powerhouse, attracting more, with 17.1%. This is further compounded by Nairobi attracting the most FDI on the continent at city level in 2015, beating Johannesburg, which has held this accolade since 2010.

With December’s data still to be recorded, Kenya is set to surpass previous years as a favoured destination for investment in Africa. With the implementation of proactive FDI legislation scheduled to be ratified during 2016 by Kenya’s government, further consolidation in 2016 is unlikely. Source: fDiMarkets

Recently while reading of Transnet’s terminal capex expansion plans, I came across this interesting if not highly improbable plan featured in an article by Harry Valentine on

Recently while reading of Transnet’s terminal capex expansion plans, I came across this interesting if not highly improbable plan featured in an article by Harry Valentine on

South Africa is moving away from a policy promoting trade and investment to one that contradicts this, a roundtable on SA-European Union (EU) trade relations heard on Tuesday.

South Africa is moving away from a policy promoting trade and investment to one that contradicts this, a roundtable on SA-European Union (EU) trade relations heard on Tuesday.

You must be logged in to post a comment.