Another Tralac sponsored publication which should be of great interest to trade practitioners, economists and investors, and agricultural specialists. Herewith the foreword to the ebook which is available for download from Tralac’s website – Click here!

The accession of South Africa into the BRICS formation has attracted a lot of attention internationally. Some welcomed the step while others questioned it. A closer look at BRICS reveals that these countries share some fundamental features while they differ in others. On that note, this book does not attempt to define BRICS.

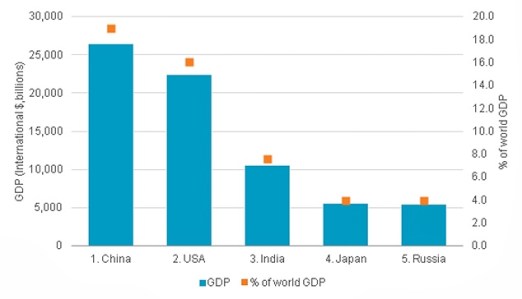

BRIC, the acronym, was coined by Jim O’Neill of Goldman Sachs in 2001. The founding members of this political formation are Brazil, Russia, India and China, aligning well with the word formulation. The formation of the BRIC was motivated by global economic developments and change in the geopolitical configurations. South Africa joined the group in 2011, thus opening the possibility of putting Africa on the BRICS’ agenda. South Africa’s admission to the group was motivated by China and supported by Russia. Its accession to the BRICS generated much discussion about the country’s suitability to be part of the formation. One of the real issues raised is that South Africa does not measure up to the other BRIC economies in terms of population, trade levels and performance, and growth rates. A formation such as the BRICS is of value to South Africa only if the country’s strategic development interests (relating, for example, to agriculture) are to be on the agenda. South Africa faces particular challenges related to market access into the BRIC countries.

BRIC, the acronym, was coined by Jim O’Neill of Goldman Sachs in 2001. The founding members of this political formation are Brazil, Russia, India and China, aligning well with the word formulation. The formation of the BRIC was motivated by global economic developments and change in the geopolitical configurations. South Africa joined the group in 2011, thus opening the possibility of putting Africa on the BRICS’ agenda. South Africa’s admission to the group was motivated by China and supported by Russia. Its accession to the BRICS generated much discussion about the country’s suitability to be part of the formation. One of the real issues raised is that South Africa does not measure up to the other BRIC economies in terms of population, trade levels and performance, and growth rates. A formation such as the BRICS is of value to South Africa only if the country’s strategic development interests (relating, for example, to agriculture) are to be on the agenda. South Africa faces particular challenges related to market access into the BRIC countries.

Agricultural issues are discussed under the Standing Expert Working Group on Agriculture and Agrarian Development. The issues that are prioritised include:

- The development of a general strategy for access to food (this is where market access needs to be tabled), which is tasked to Brazil

- Impact of climate change of food security, which is allocated to South Africa

- The enhancement of agricultural technology, cooperation and innovation that is allocated to India

- Creation of an information base of BRICS countries that is allocated to China

In 2012, at the annual conference of the Agricultural Economics Association of South Africa, the National Agricultural Marketing Council (NAMC) co-hosted a workshop aimed at establishing a dialogue on how agriculture can benefit from South Africa’s membership of the BRICS. It came out clearly from the workshop that agriculture needs to be better positioned to benefit from the BRICS formation. One important issue that was noted was that market access for South African agricultural produce into the BRICS countries could be improved. In this regard, an honest question was raised whether, as the country’s agriculture stakeholders, we fold our arms and do nothing since this this is a political formation (while market access is an economic issue), or whether we use this political formation to address our socioeconomic issues as they relate to these countries. Market access is one of the issues of interest to South Africa’s agriculture industry within the BRICS formation, together with issues such as the diffusion of technologies and collaborations.

The research that is presented in this book addresses a range of important issues related to the trade and investment relations among these countries. The performance of their agricultural sectors as well as trade amongst these countries is also examined. There is also focus on the relationship between BRICS and Africa, and what this means for South Africa’s trade relations with other African countries. Source: Tralac

![Delegates who attended the first BRICS Customs Heads of Customs Meeting [SARS]](https://mpoverello.com/wp-content/uploads/2013/03/delegates-who-attended-the-first-brics-customs-heads-of-customs-meeting-sars_snapseed.jpg)

You must be logged in to post a comment.